DIFFERENT TYPES OF NBFC REGISTRATIONS & ITS PURPOSES

A Non-Banking Financial Company (“NBFC”) in India is a company registered under the Companies Act, 2013, who has received the Certificate of Registration (CoR) from the Reserve Bank of India (“RBI”) under Section 45-IA of the RBI Act, 1934, thereby recognizing them as the regulated entity.

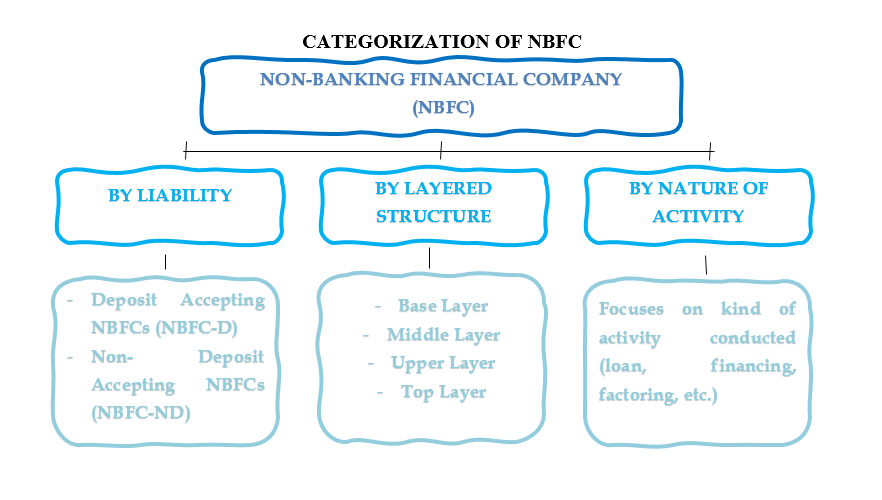

NBFCs play a crucial role in India’s financial ecosystem: they complement banks, provide targeted credit solutions and help deepen financial inclusion by reaching segments often underserved by traditional banking. Given their diverse business models and risk profiles, NBFCs are further categorized and registered into specific types based on liability structure, size and systemic importance and nature of activity. This detailed classification ensures appropriate regulatory oversight tailored to their operations.

This article elaborates on these types of NBFC registrations and the purpose behind each category, highlighting why such nuanced categorization strengthens financial stability, protects consumers, and drives economic growth.

NBFCs are primarily divided into those permitted to accept public deposits and those prohibited from doing so. This classification helps balance depositor protection with financial intermediation.

| NBFC REGISTRATION AND ITS PURPOSE BASED ON LIABILITY | ||

|---|---|---|

| Type of NBFC | Registration required | Purpose of registration |

| Deposit Accepting NBFCs (NBFC-D) | Specifically authorised to accept public deposits from individuals or entities. These NBFCs are to be registered as NBFC-D. These deposits may include term deposits, recurring deposits, etc. NBFC-Ds operate under stricter regulatory norms. | To mobilize funds directly from the public and deploy them into lending, asset finance, infrastructure finance, or other permitted financial activities. As they handle public money, NBFC-Ds are subject to stricter prudential norms, including higher capital adequacy, exposure norms, deposit insurance, asset liability management (ALM), and mandatory credit ratings. |

| Non-Deposit Accepting NBFCs (NBFC-ND) | These NBFCs though registered with the RBI, cannot accept deposits from the public. They fund their lending and investment activities mainly through equity, debt instruments, bank borrowings, and institutional funding rather than retail public deposits. | To provide credit, finance, and investment services to businesses and individuals without depending on public deposits, thus reducing systemic risk. NBFC-NDs have lenient regulatory requirements compared to NBFC-Ds. However, large NBFC-NDs classified as NBFC-ND-SI (Systemically Important, with asset size more than Rs. 500 crore) must comply with stricter norms such as capital adequacy, corporate governance, exposure limits, etc. to mitigate financial stability risks. |

Under the RBI’s Scale-Based Regulation (SBR) framework introduced in 2023, NBFCs are classified into layers based on size, complexity and systemic importance. This layered framework ensures that regulation scales with risk and systemic relevance.

| NBFC REGISTRATION AND ITS PURPOSE BASED ON LAYERED STRUCTURE | ||

|---|---|---|

| Type of NBFC | Registration required | Purpose of registration |

| Base Layer (NBFC-BL) | Non-deposit taking NBFCs with asset size below Rs. 1,000 crore and other NBFCs (e.g., smaller NBFCs, NBFC-P2P, NBFC-AA, NBFCs not availing public funds and not having customer interface) must register under Section 45IA of the RBI Act under this category. | To allow smaller NBFCs to operate with lighter regulatory requirements while ensuring governance, prudential norms, and consumer protection. |

| Middle Layer (NBFC-ML) | All deposit-accepting NBFCs (NBFC-D); large non-deposit taking NBFCs (asset size Rs. 1,000 crore or more) and specific NBFCs such as HFCs, IFCs, CICs, SPDs, etc. | To strengthen supervision over entities with systemic impact by applying stricter prudential norms, capital adequacy, and governance standards. |

| Upper Layer (NBFC-UL) | NBFCs specifically identified by RBI as systemically significant (based on size, complexity, and interconnectedness). | To apply bank-like regulation including tighter governance, risk management, differential provisioning, mandatory listing, and dedicated board committees. |

| Top Layer (NBFC-TL) | Empty by design; populated only if RBI identifies NBFCs with exceptionally high risk profile. | To impose very stringent, tailored regulations to protect financial stability in exceptional circumstances. |

Based on nature of activity the special registrations enumerated hereunder ensures that NBFCs operate within well-defined mandates, reflecting their business models:

|

NBFC REGISTRATION AND ITS PURPOSE BASED ON NATURE OF ACTIVITY |

||

|

Type of NBFC |

Registration required |

Purpose of registration |

|

Investment and Credit Company (ICC) |

Registration with RBI as NBFC-ICC |

To carry on the principal business of asset finance, lending (other than its own activity) and acquisition of securities; not covered under other specific NBFC categories. |

|

Housing Finance Company (HFC) |

NBFCs with at least 60% of total assets in housing finance (at least 50% for individuals) shall be registered with National Housing Bank (NHB) / RBI under HFC regulations |

To primarily provide finance for housing; ensure that significant part of total assets and lending is directed towards housing, especially to individuals. |

|

Infrastructure Finance Company (IFC) |

Registration with RBI as NBFC-IFC is necessary for NBFCs who deploy at least 75% of total assets towards infrastructure lending. |

To channel long-term funds to infrastructure projects critical for economic development. |

|

Infrastructure Debt Fund (IDF-NBFC) |

Registration with RBI as non-deposit taking NBFC-IDF. |

To refinance completed infrastructure projects post-COD, and directly finance TOT projects, supporting long-term infrastructure funding. |

|

Core Investment Company (CIC) |

Registration as CIC is required for NBFCs meeting specific criteria: 90% or more of net assets in group shares/securities; more than or equal to 60% in equity/InvITs as sponsor; having asset size more than or equal to Rs. 100 crore; accepts public funds; does not trade except block sale for disinvestment; limited financial activities as specified. |

To hold and manage investments in group companies without trading; ensure systemic oversight of large, group-focused investment entities. |

|

Micro Finance Institution (NBFC-MFI) |

Non-deposit taking; having 75% or more of total assets deployed as collateral-free loans to households with annual income less than or equal to Rs. 3,00,000; providing flexible repayment options and no lien on borrower’s deposit shall be registered with RBI as NBFC-MFI |

To provide collateral-free microfinance loans to low-income households and support financial inclusion and access to small credit. |

|

NBFC-Factors |

Non-deposit taking NBFC; NBFCs having 50% or more of total assets in factoring business; or 50% or more of gross income from factoring should obtain registration with RBI as NBFC-Factor |

To focus on receivables financing, improving SMEs’ liquidity. |

|

Mortgage Guarantee Companies (MGC) |

RBI Registration is required for NBFCs which provides mortgage guarantees and whose more than equal to 90% of turnover or gross income arise from mortgage guarantee business. |

To offer mortgage guarantees covering repayment of housing loans, housing credit markets. |

|

Standalone Primary Dealers (SPDs) |

Authorization and registration with RBI as SPD are to be undertaken by primary dealer in Government Securities; persons who participate in primary auctions, market making in G-Secs, maintain investment and turnover obligations. |

To act as market makers in G-Sec market, enhancing depth and liquidity in government securities market. |

|

Non-Operative Financial Holding Company (NOFHC) |

Registration with RBI under licensing guidelines for new private banks. |

To hold shares of a bank and other financial service companies in a group, ensuring separation of banking and other financial services businesses. |

|

NBFC – Account Aggregator (NBFC-AA) |

NBFCs who Collects, retrieves, consolidates and presents customer’s financial information to the customer or financial information users and such data is not owned by aggregator shall mandatorily obtain registration with RBI as NBFC-AA |

To collect and securely share consumer consented financial data to financial information users; enabling better financial services. |

|

NBFC – Peer to Peer Lending Platform (NBFC-P2P) |

NBFC shall be registered with RBI as NBFC-P2P if it provides an online or digital platform to facilitate peer-to-peer loans between participants. |

To facilitate digital peer-to-peer loans between borrowers and lenders offering alternative credit access and digital lending. |

The detailed registration framework for NBFCs – based on liability, regulatory layer and nature of activity – is not just a compliance requirement. But reflects the multi-layered, specialised and dynamic role NBFCs play within India’s financial system. This structure ensures:

- Protection of depositors and investors

- Risk-sensitive regulation for systemically important entities

- Encouragement for specialised NBFCs to serve niche sectors (housing, infrastructure, microfinance, digital data, etc.)

Collectively, these diverse NBFCs fill vital credit gaps, support entrepreneurship, promote priority sector lending, and deepen financial inclusion. By aligning regulation with business models and risk profiles, India’s NBFC registration framework effectively balances innovation and growth with stability and consumer protection.

Further, once an NBFC is successfully registered and has obtained a Certificate of Registration from RBI, it must ensure that other key registrations and approvals essential for its operations are obtained.

For a detailed understanding of these additional registration requirements, please refer to our article Compliance Roadmap for Newly Registered NBFCs at https://nbfcadvisory.in/compliance-roadmap-for-newly-registered-nbfcs/

Disclaimer: This article provides general information existing at the time of preparation and we take no responsibility to update it with the subsequent changes in the law. The article is intended as a news update and Affluence Advisory neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this article. It is recommended that professional advice be taken based on specific facts and circumstances. This article does not substitute the need to refer to the original pronouncement.