Investment and Credit Company (NBFC-ICC)

Microfinance Company (NBFC-MFI)

Infrastructure FinanceCompany (NBFC-IFC)

Factoring Company (NBFC-Factor)

Housing FinanceCompanies (NBFC-HFC)

Core Investment Company (NBFC-CIC)

Account Aggregators (NBFC-AA)

Peer to Peer LendingPlatforms (NBFC-P2P)

Infrastructure Debt Fund NBFC (IDF-NBFC)

Mortgage Guarantee Companies (MGC)

Investment and Credit Company (NBFC-ICC)

NBFC-ICC is a financial institution carrying on as its principal business – asset finance, the providing of finance whether by making loans or advances or otherwise for any activity other than its own and the acquisition of securities; and is not any other category of NBFC as defined by RBI in any of its Master Directions.

Get Started with Affluence

Microfinance Company (NBFC-MFI)

NBFC-MFIs are financial institutions that support poor and vulnerable sections of society. They offer small loans, savings, and other financial products that could be of help to the people. Microfinance on the other hand benefits people who do not have access to traditional banking services. These services help small vendors who wish to expand their business using microloans or savings products to promote financial resilience.

Get Started with Affluence

Infrastructure FinanceCompany (NBFC-IFC)

This type of NBFC invests at least 75% of its assets in infrastructure loans and must maintain a minimum Net Owned Fund of ₹300 crores. It is required to have a credit rating of at least “A” or an equivalent Capital to Risk-Weighted Assets Ratio (CRAR) of at least 15%. Notable companies in this category, such as GMR Infrastructure Ltd. and Hindustan Construction Company, primarily engage in providing infrastructure finance through loans.

Get Started with Affluence

Factoring Company (NBFC-Factor)

NBFC-Factor is primarily engaged in thebusiness of factoring.Factoring is an important source of liquidity worldwide, especially for MSMEs. Factoring is a transaction where an entity sells its receivables (dues from a customer) to a third party (a ‘factor’ like a bank or NBFC) for immediate funds. All or part of the invoice can be sold to a factor to get money immediately at

a competitive interest rate. The factor then collects payments from the buyer of goods and earns a commission in the form of some interest. This is different from bill discounting. In bill discounting, a bank or NBFC gives a certain percentage of the total outstanding value of invoices to the seller, and in most cases, the seller has to take on the responsibility for payment of invoices by the buyer to the factor(Recourse Bill Discounting). However, in the case of factoring, the factor takes responsibility for collecting invoices.

Get Started with Affluence

Housing FinanceCompanies (NBFC-HFC)

Housing finance companies (HFCs) are organisations registered under the Companies Act. They are primarily engaged in providing loans or finance for housing purposes through direct or indirect means. Earlier regulated by the National Housing Bank (NHB), HFCs’ regulation was transferred to the Reserve Bank of India (RBI) in 2019 through amending the statutes by the government. However, a few of their regulatory powers are still with NHB.HFCs were introduced with the idea of freeing up Indian banks with increasing liabilities. They shared the housing loan portfolio and made the credit facility easier for each income group.

Get Started with Affluence

Core Investment Company (NBFC-CIC)

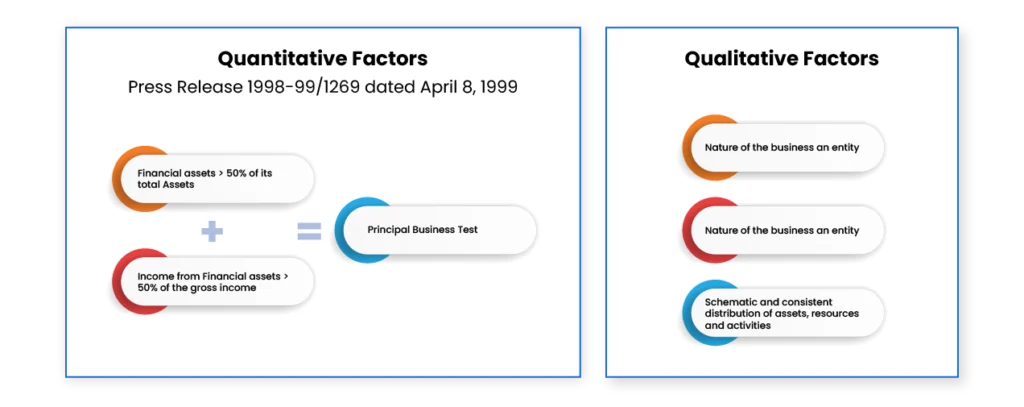

NBFC-CIC is a specialized NBFC with an asset size of above Rs 100 crore. According to an RBI circular dated December 20, 2016, a CIC’s main business is the acquisition of shares and securities with certain conditions. One of the conditions stipulated by the central bank is that the CIC holds not less than 90 percent of its net assets in the form of investment in equity shares, preference shares, bonds, debentures, debt or loans in group companies.

CICs with an asset size above Rs 100 crore are regulated by central bank laws. CICs that have an asset size below Rs 100 crore are exempted from registration and regulation from the Reserve Bank, except the CICs that have overseas investments in the financial sector.

Get Started with Affluence

Account Aggregators (NBFC-AA)

Account Aggregators (AA) are non-banking financial companies, licensed by RBI, that act like a bridge, to deliver data from Financial Information Providers (FIP) that hold your personal or corporate financial data to Financial Information Users (FIU) that are providing financial services to you.Account Aggregator replaces the long terms and conditions form of ‘blank cheque’ acceptance with a granular, step by step permission and control for each use of your data.

Get Started with Affluence

Peer to Peer LendingPlatforms (NBFC-P2P)

NBFC-P2P are online platforms that facilitate borrowing and lending directly between individuals (borrowers) and investors (lenders), bypassing traditional financial intermediaries like banks and financial institutions. In India, these platforms are regulated by the Reserve Bank of India (RBI) under the NBFC-P2P (Non-Banking Financial Company – Peer to Peer) framework.

These platforms offer an alternative to traditional lending methods and have gained popularity due to their ability to offer higher returns for investors and quicker, more flexible loans for borrowers.They provide various loan options, including secured and unsecured loans, and are often used by individuals with a poor credit score or businesses that need immediate financing.

Get Started with Affluence

Infrastructure Debt Fund NBFC (IDF-NBFC)

IDF-NBFC are financial vehicles designed to provide long-term debt financing to infrastructure projects, particularly to reduce the financing gap for infrastructure development.

Their primary purpose is to attract long-term capital from institutional investors such as pension funds, insurance companies, and sovereign wealth funds for funding infrastructure projects in India.

Get Started with Affluence

Mortgage Guarantee Companies (MGC)

MGC is a specialized financial institution that provides mortgage guarantee services to lenders (such as banks and financial institutions) in case a borrower defaults on their mortgage loan. This guarantee helps protect lenders from the risk of non-payment of home loans or other types of secured loans, especially in the event of default by the borrower.

For MGC at least 90% of the business turnover or at least 90% of the gross income is from the mortgage guarantee business, and the net owned fund is Rs 100 crore.

Get Started with Affluence

+91 859 116 7727

+91 859 116 7727  connect@affluence.net.in

connect@affluence.net.in