- Sun-Tue (9:00 am-7.00 pm)

-

+91 859 116 7727

+91 859 116 7727

-

connect@affluence.net.in

connect@affluence.net.in

The microfinance segment in India has proved to be fundamental for promoting financial inclusion by extending credit to low-income groups that are traditionally not catered to by lending institutions. The essential features of microfinance loans are that they are of small amounts, with short tenures, extended without collateral and the frequency of loan repayments is greater than that for traditional commercial loans. These loans are generally taken for income-generating activities, although they are also provided for consumption, housing and other purposes. There exist various market players in the microfinance industry viz. scheduled commercial banks, small finance banks, co-operative banks, various NBFCs extending microfinance loans and NBFCs-MFIs.

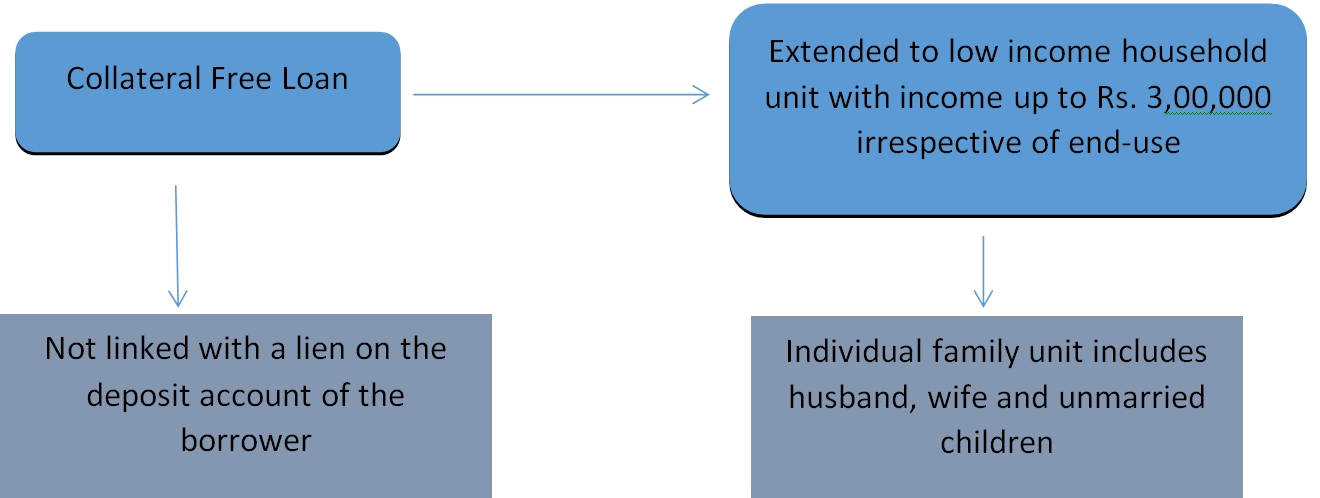

As per the RBI Master Direction – Reserve Bank of India (Regulatory Framework for Microfinance Loans) Directions, 2022, a microfinance loan is defined as follows:

Reserve Bank of India (Regulatory Framework for Microfinance Loans) Directions, 2022

A “NBFC-MFI” means a non-deposit taking NBFC which has a minimum of 75 percent of its total assets deployed towards “microfinance loans”.